1. Coronavirus will pass, whereas fiscal and monetary stimulus will be long-lasting

- » Bond yields are likely to remain low for many years from now, with base rates at all time lows and extensive central bank bond purchases (quantitative easing). The US Federal Reserve effectively announced unlimited QE a few days ago.

- » Governments worldwide are increasing expenditure to extreme levels that have historically only occurred at times of war, representing 10% of GDP in the US and as much as 20% in the UK, with more likely to come.

- » These stimulus measures will ripple through the global economy for years to come, driving a strong growth recovery once coronavirus is beaten, while reducing the risks of widespread corporate defaults and supporting higher valuation multiples for equity markets.

2. The best returns tend to come from the point of greatest pessimism

- » As Warren Buffet famously said, investors should be “fearful when others are greedy and greedy when others are fearful.” One must remember that the value of an equity stake in a business is the present value of all future cashflows, not just those over the next few months.

- » The best rolling ten-year equity market returns, measured by the Dow Jones Industrial Average index, have come from the times when all hope seemed lost. Investors buying equities at these points – including at the end of WW1 and WW2, at the depth of the great crashes of 1932 and 2009, and after Black Monday in 1987 – benefited from 10 year annualised returns of 10-15% per annum.

- » Several of our underlying managers are seeing incredible value on offer following the market falls, with estimates of upside potential climbing to levels not seen since the global financial crisis.

3. Markets will recover long before the economic and humanitarian crisis is over

- » Financial markets always move to reflect a change in the outlook for economies and corporate profitability well ahead of the fundamentals actually reflecting that. This ‘lead’ effect means that declines in global growth and corporate earnings, as well as a rise in defaults, are already very much ‘priced in’ at this point.

- » This means markets have potential to recover significantly if the actual outcome is simply not as bad as expected. Markets are already discounting much of the grim news which bombards us daily and, while the news flow is unlikely to improve for some time, they will almost certainly begin to recover well before the worst of the economic and humanitarian impact is felt.

- » The Chinese equity market has been a perfect example of this. While the coronavirus was treated as an isolated issue for China in January and February, the market bottomed in early February around the time the spread of the virus peaked and began to slow down. The Chinese equity market subsequently fell further in recent weeaks due to the weaker outlook for growth outside of China, but as of today it is still by far the best performing major market globally year to date.

- » Similarly, we expect global markets to begin their recovery once an end is in sight, well before it is reached. We are already seeing signs of that in Europe, with the growth in new cases beginning to slow down. Interestingly, European equity markets are up over 6% since 13th March, while the US market is down nearly 9%.

4. Market falls should be welcomed by long term investors

- » As painful as large market declines can feel at the time, the effect on valuation statements are only temporary, so long as investors don’t crystallise their losses.

- » For those making regular savings, or with additional reserves to invest, lower valuations mean more shares/units can be acquired for any given cost. This ‘dollar cost averaging’ effect creates greater value over the long run.

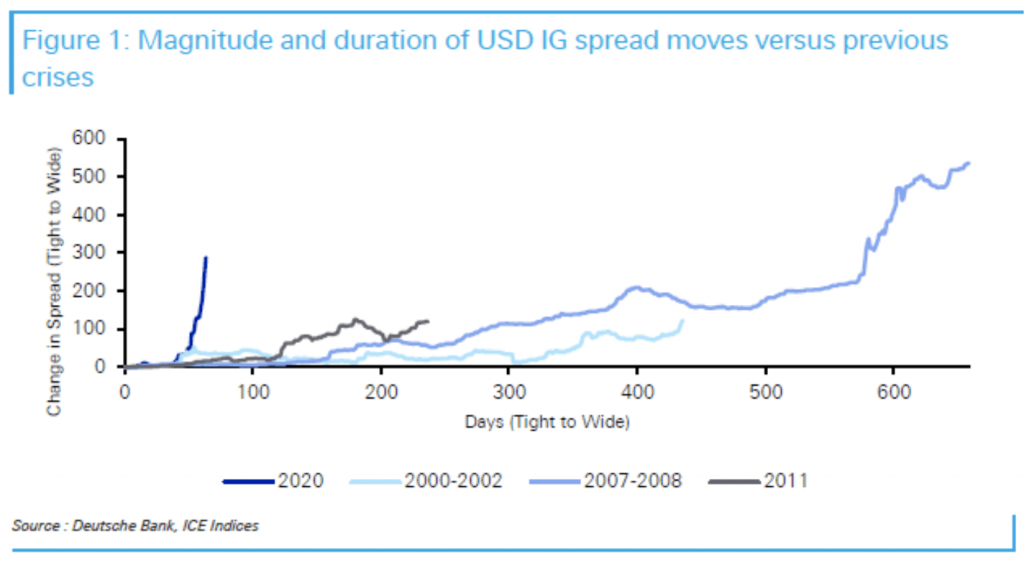

- » Most equity market investors are well paid to wait for any recovery, as well. For example, the dividend yield on the FTSE 100 index is now in excess of 6% per annum. Fixed income investors are also well paid, with high-grade corporate bond indices offering yields in excess of 4%, compared to bank deposit rates of zero or less in most countries. The chart below shows how extreme the market reaction has been compared to other bear markets, demonstrated by the speed and magnitude of the increase in spreads on USD investment grade bonds (the excess yield over government bonds)

5. The Harmony Portfolios are well positioned to capture a market recovery

- » The Portfolios came into this period carrying less risk than at most times over the last five years. We recognised that valuations were relatively high and that markets were vulnerable to a substantial correction. In recent years we had reduced our equity and credit market exposure and built up holdings in defensive asset classes (including government bonds, gold and alternatives).

- » This has helped moderate losses in recent weeks, while our multi asset-class diversification has ensured the Portfolios held up better than many single asset class strategies and indices. Importantly, we have capacity to increase our equity and credit holdings, whilst remaining within our mandates, which will enable the Portfolios to deliver higher returns when markets recover.

- » We increased risk to good effect after sharp equity market declines in 2015 and 2018. This time around, we have been right (so far) not to increase our equity holdings, as we recognised that the worst was yet to come in markets. We have maintained our exposure though, through rebalancing rather than the alternative of letting allocations drift, thus ensuring we will get full benefit of any eventual market rebound.

6. The Harmony Portfolios are fully liquid

- » All Harmony Portfolios are fully liquid. That means we offer daily pricing and daily dealing for investors, no matter what the market conditions are. Furthermore, we ensure we are always able to adjust portfolios for subscriptions or redemptions, by only buying underlying investments that are also fully liquid (i.e. no liquidity mismatch).

- » The

liquid nature of the portfolio holdings has led to greater downside in

recent weeks; as liquidity

was sucked out of markets and investors panicked, liquid investments inevitably bore the brunt of the selling pressure. However, this is a temporary ‘mark to market’ phenomenon, and prices will recover as supply and demand come back into balance. - » The benefits of liquidity at this time are twofold and neither should be underestimated. Investors in the Harmony Portfolios can redeem their holdings at any time, or equally they can add to their holdings to take advantage of the exceptional value on offer in equity and credit markets.

7. This market environment is well suited to a multi-asset and active approach

- » The levels of indiscriminate selling and deleveraging we have observed have created wide ranging opportunities across markets. Most defensive sectors and stocks have fallen as much as markets more broadly, meaning prices have fallen far further than justified by any deterioration in fundamentals, creating an opportunity to buy high quality assets at substantial discounts to their fair value.

- » Active managers are able to take full advantage of these dislocations, while passive strategies, by definition, will not actively tilt towards the mispriced opportunities. Furthermore, the flaws inherent in passively managed credit ETFs have been highlighted recently; they have provided liquidity but at huge cost, with material discounts to NAV opening up. The vast majority of equity and credit holdings in the Harmony Portfolios are in actively managed strategies, meaning they are carefully researched and selected by many of the world’s best specialists in those areas.

- » Correlations

between asset classes have been unusually high, meaning the

diversification benefits

of our multi-asset class approach have not been felt as much as they usually are through periods of heightened volatility. However, when markets stabilise, as they have shown some early signs of doing in recent days, then prices should begin to realign with fundamentals and performance should rebound strongly.